Your UK Commercial Lease Agreement Explained

A commercial lease agreement template is your blueprint for renting a business space, setting out the legal relationship between a landlord and tenant. Let's break down this crucial document and turn it from a complex legal hurdle into a powerful tool for securing your business’s physical home.

Your Blueprint for Securing a Business Space

Think of a commercial lease like the architectural plan for your business premises. You wouldn't build a property without a solid blueprint, and you definitely shouldn't rent one without a clear, comprehensive agreement in place. This guide is here to demystify what can often feel like an intimidating legal document, making it a practical tool for both tenants and landlords.

Starting with a professionally drafted commercial lease template is one of the smartest moves you can make. It saves time, money, and a world of future headaches. In the UK's competitive property market, getting this right from day one is your best defence. After all, leasing is overwhelmingly the norm; a staggering 94.9% of UK organisations lease their main commercial space rather than owning it. That statistic alone shows just how vital a solid lease agreement is to the way business gets done today.

A good template isn't just about plugging in names and numbers. It provides a solid foundation, ensuring every critical detail is covered. It's about much more than just the rent; it’s about creating a stable, predictable environment where your business can thrive.

The Foundation of a Strong Lease

A strong lease begins long before you sign on the dotted line. It starts with clear intentions and a shared understanding of the core terms, setting the stage for a positive landlord-tenant relationship from the get-go.

For many, this process kicks off with a preliminary document that outlines the main points of the deal. It acts as an initial handshake, ensuring both sides are on the same page about rent, the length of the lease, and key responsibilities before you dive into the full agreement. If you’re at this stage, you might find it helpful to learn how a Letter of Intent can lay the groundwork for your lease negotiations.

A great lease is built on clarity. It removes ambiguity and provides a clear roadmap for the entire tenancy, protecting both the landlord's asset and the tenant's business operations.

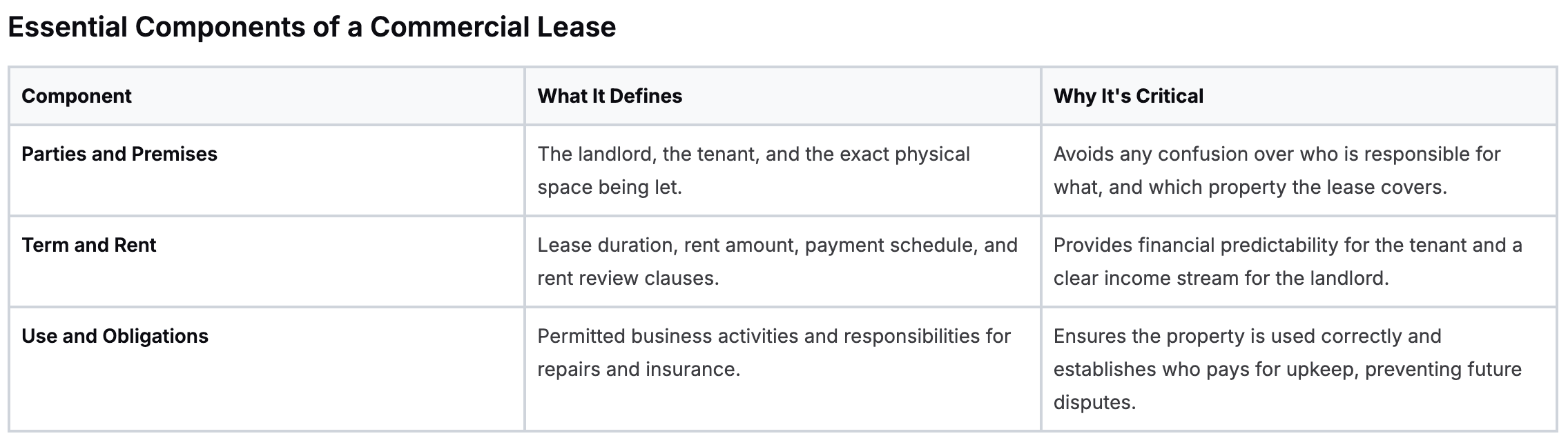

So, what are the absolute essentials? Before diving into the finer details, every commercial lease must clearly define a few non-negotiable elements. Think of these as the structural pillars of your agreement.

Here’s a quick rundown of the components that form the backbone of any commercial lease.

By carefully reviewing each of these foundational elements from the start, you can build an agreement that not only offers strong legal protection but also supports your long-term financial stability. It’s the key to ensuring your business has a secure home to grow.

What a Commercial Lease Agreement Really Does

Let's cut through the dense legal jargon. At its heart, a commercial lease agreement is the official rulebook for renting a business property. It's a legally binding contract that gives a tenant the right to use a space for business, while also protecting the landlord’s major financial stake in that property.

It's vital to realise this document is nothing like the residential lease you might sign for a flat. Thinking they're similar is a common and often very costly mistake. While both involve renting, their purpose, flexibility, and the responsibilities they place on you are worlds apart.

More Than Just a Tenancy

A residential lease is usually a standard, one-size-fits-all document. Think of it like a standard car hire agreement; the terms are mostly fixed, and consumer protection laws are strong. The landlord is almost always responsible for big repairs, the building's structure, and making sure the property is habitable.

A commercial lease, on the other hand, is like custom-building a long-term vehicle lease just for your business. It’s built on the assumption that both sides are savvy business people.

A commercial lease agreement operates on the principle of caveat emptor, or 'let the buyer beware'. The law offers far fewer automatic protections for business tenants, which puts huge importance on the negotiated terms written into the contract itself.

This single difference has massive, real-world consequences. The terms are highly negotiable, and the responsibilities passed to the tenant are far greater. This is precisely why a generic form won't do the job and why a proper commercial lease agreement is the only sensible starting point for any UK business.

Key Distinctions from Residential Leases

Understanding these specific differences is crucial before you even start looking at properties. The expectations and financial duties are completely different.

Here are the main areas where commercial and residential leases go their separate ways:

- Longer Terms: Commercial leases often run for three to ten years or even longer, a far cry from the usual one-year term for a flat. This offers stability for your business, but it's also a much bigger financial commitment.

- Greater Responsibility: In many commercial leases, especially 'net leases', you're on the hook for costs well beyond the basic rent. This can include property taxes, building insurance, and even structural repairs—expenses almost always covered by the landlord in a residential setting.

- Negotiation Flexibility: Almost every clause in a commercial lease is up for negotiation. This covers everything from the rent and review schedules to break clauses (your option to end the lease early) and what you're allowed to use the property for.

- Business-Specific Clauses: These agreements are filled with clauses that simply don’t appear in residential leases. You'll find terms covering signage, subletting to another business, alterations for your specific fit-out, and even your operating hours.

Getting your head around these differences is the first step to securing a deal that works for you. It shows why you can't walk into a commercial letting with a residential mindset. Every single clause has to be carefully weighed for its long-term impact on your business's bottom line and day-to-day operations.

Finding the Right Type of Commercial Lease

Signing a commercial lease isn't just about agreeing on the monthly rent. The type of lease you choose can have massive, long-term financial impacts on your business, as it dictates exactly who is responsible for all the extra costs beyond the rent itself. Getting this wrong from the start is a costly mistake.

It helps to think of it like booking a holiday. You could go for an all-inclusive package where one fee covers everything from flights to food. Or, you might prefer a self-catering apartment where you pay a base price and cover all your own expenses. Commercial leases follow a similar logic, and your choice will shape your monthly budget and responsibilities.

The All-Inclusive Option: The Gross Lease

A Gross Lease is the simplest of the bunch, making it a very predictable option for tenants. This works just like that all-inclusive holiday; you pay one single, flat rental fee, and the landlord handles almost all of the property’s running costs.

These operating expenses usually include:

- Property taxes

- Building insurance

- Common area maintenance (CAM) charges

- In some cases, even utilities

The main draw for tenants is budget certainty—your primary cost is fixed, making financial planning much easier. Of course, landlords aren't taking on this risk for free. They price this convenience into the agreement, which means the base rent is typically higher than with other lease types. It's a great fit for businesses that value straightforward, consistent payments above all else.

The Pay-As-You-Go Approach: Net Leases

On the other end of the spectrum, Net Leases shift some, or even all, of the operating expenses onto the tenant. Think of this as a pay-as-you-go mobile plan; your base cost is lower, but you're responsible for your own usage. In exchange for shouldering more financial risk, your base rent will be significantly lower.

There are three main types of net lease, with each "net" adding another layer of expense for the tenant to cover.

- Single Net (N) Lease: The tenant pays the base rent plus their share of the property taxes. The landlord still covers other big costs like insurance and maintenance.

- Double Net (NN) Lease: Here, the tenant is responsible for base rent, property taxes, and the building's insurance premiums. The landlord usually only remains on the hook for major structural repairs and common area upkeep.

- Triple Net (NNN) Lease: This is the go-to lease for most freestanding commercial buildings. The tenant pays the base rent plus all three of the major operating costs: property taxes, building insurance, and all maintenance costs, including structural ones.

A Triple Net (NNN) lease gives landlords a passive, hands-off investment and tenants a great deal of control over the property. However, it also comes with the highest level of financial risk for the tenant. An unexpected roof repair or boiler failure becomes your problem to pay for.

The Retail Favourite: The Percentage Lease

You'll most often find a Percentage Lease in retail settings like shopping centres and high streets. In this arrangement, the tenant pays a lower-than-market base rent, plus an agreed-upon percentage of their gross sales revenue once it crosses a certain threshold.

This structure effectively creates a partnership. The landlord has a direct incentive to keep the property attractive and drive footfall because when their tenants succeed, their own income increases. For a new shop, the low initial rent can be a lifeline, but you need to be ready for your rent to climb as your business grows.

Commercial Lease Types: Landlord vs Tenant Costs

To help you visualise how these costs are divided, let's break down who typically pays for what under each structure.

This table makes it clear how the financial responsibility shifts from the landlord to the tenant as you move from a Gross to a Triple Net lease. The lower base rent of a net lease can be tempting, but it requires careful budgeting for those additional, often variable, costs.

Ultimately, choosing the right lease demands a clear-eyed look at your business model, how much risk you're willing to take on, and how much control you want over the building. Understanding these fundamental differences is the first critical step toward securing a lease that truly works for you.

Here is the rewritten section, crafted to sound human-written and match the provided examples.

Breaking Down Your Commercial Lease Clause by Clause

Ever looked at a commercial lease and felt like you were trying to read another language? It’s a document packed with legal jargon that will define your business life for years. But figuring out these clauses isn't just a job for solicitors; it's absolutely vital for anyone putting their name on the dotted line.

Think of the lease as the rulebook for your business premises. Getting your head around the details now can save you from huge headaches and costly arguments down the road. Let's walk through the most important parts of a typical UK commercial lease and translate them into plain English.

The Core Components: Parties and Premises

Every lease kicks off by identifying who's involved and what's being rented. It sounds simple, but getting this bit wrong can make the whole contract unenforceable.

- Parties: This clause clearly names the landlord (the property owner) and the tenant (you, the business renting the space). It’s crucial that the full, correct legal names are used for everyone involved.

- Premises: This defines the exact physical space you're renting. It needs to be more than just an address. Look for details like the floor, the unit number, and a plan that clearly shows the boundaries. Any vagueness here can lead to arguments over who controls shared hallways or that patch of land out back.

The Financial Heartbeat: Rent and Rent Reviews

This is the part everyone flips to first, and for good reason—it’s all about the money. The rent clause sets out how much you’ll pay, how often (usually quarterly in advance), and on what date.

But the starting rent is only half the story. The rent review clause is just as important because it dictates how your rent can go up during the lease. If your lease is for more than a couple of years, you can bet one of these will be in there.

A rent review clause lets the landlord adjust your rent to match current market prices. If you don't pay attention to how it's worded, you could be hit with massive, unpredictable rent increases later on.

In the UK, rent reviews usually happen in one of three ways:

- Open Market Rent Review (OMRR): This is the most common. Your rent is adjusted to what a new tenant would pay for a similar property in the same area. It’s fair in theory, but it can be volatile if the market shoots up.

- Index-Linked Review: The increase is tied to an inflation index, like the Retail Price Index (RPI). This gives you a much better idea of what to expect, making it easier to budget.

- Fixed Increases: The lease sets out specific, pre-agreed increases on certain dates. This is the most predictable option for both you and the landlord.

Defining Your Business Activities: Permitted Use

The permitted use clause is one of the most restrictive in any lease. It specifies exactly what you can do in the property, often in very narrow terms, like "use as a retail shop for selling books and for no other purpose."

This protects the landlord, who needs to make sure your business won't cause problems for other tenants or violate local planning rules. For you, it's critical that this clause is broad enough for your business to operate and even grow. If you decide to start selling coffee in your bookshop, you could be in breach of your lease if it’s not covered.

Keeping the Property in Shape: Repairing Obligations

This is where so many landlord-tenant disputes begin. The repairing obligations clause lays out who has to fix what. Many UK leases are Full Repairing and Insuring (FRI), which puts the responsibility for all repairs—from a leaky tap to a damaged roof—squarely on the tenant.

This means you could be on the hook for major, expensive work. Before you sign anything, get a professional survey done. You can then attach a "schedule of condition" to the lease, which is just a detailed record of the property's state with photos. This limits your repair duties, ensuring you only have to give the property back in the same condition you found it in, not better. Sometimes, a landlord will also ask for a guarantee to back up these obligations. It’s worth understanding what a Lease Guarantee involves, as it can affect your personal liability.

Making Changes and Making an Exit

Two final clauses you absolutely need to understand are alterations and breaks. They determine how much freedom you really have.

Alterations Clause: Want to paint the walls a new colour or put up a partition? This clause tells you what changes you can make. It usually forbids major structural changes but might allow cosmetic ones with the landlord's written permission. Always check before you get the builders in.

Break Clause: This is your early exit strategy. It’s an option—usually for the tenant, but sometimes for the landlord—to end the lease before the full term is up. The clause will state a specific date when you can use it, but it comes with very strict conditions. You’ll need to be fully paid up on rent, have met all your repair duties, and leave the property completely empty. Messing up even one of these tiny details can mean your break notice is invalid, and you’re stuck in the lease.

How to Tailor Your Lease for UK Businesses

A commercial lease template is a great foundation, but it’s never a one-size-fits-all solution. Think of it like a good suit off the rack—it gives you the right shape, but you’ll need a tailor to make it fit your business perfectly. This customisation is absolutely crucial in the UK, where specific laws and common practices can dramatically affect your rights.

Just filling in the blanks on a generic form is a risky move. A standard template simply can't predict the unique operational needs of your business. By tailoring the lease, you ensure it doesn’t just protect the landlord but actually works for you, supporting your day-to-day operations and future growth. This is how a simple document becomes a real business asset.

Defining Your Operational Boundaries

One of the first places to focus your attention is the ‘Permitted Use’ clause. A template might offer a vague, general definition, but you need to be specific. After all, the requirements for a quiet accountancy firm are a world away from a bustling restaurant needing special ventilation, late-night hours, and specific waste disposal.

If this clause is too narrow, it can seriously box you in. Imagine you run a coffee shop and later want to start hosting evening events or selling merchandise. A tightly written ‘Permitted Use’ clause could mean you’re suddenly in breach of your lease. You need to negotiate a definition that covers what you do now and how your business might realistically evolve in the future.

Negotiating Rent Reviews and Financial Terms

The ‘Rent Review’ clause is another area that demands careful negotiation. Many templates default to an open market rent review, but that can throw a spanner in the works of your financial forecasting. As a tenant, it pays to explore alternatives that give you more predictability.

Try to negotiate for one of these more stable methods:

- Index-Linked Reviews: Tying any rent increases to a recognised measure like the Consumer Price Index (CPI) makes the process transparent. It removes the uncertainty and potential for disputes that often come with open market valuations.

- Fixed Increases: Agreeing on set percentage or pound-amount increases at specific dates gives you complete budget certainty. For a new or growing business, this is often the most straightforward and stable option.

Understanding Your Rights Under UK Law

For any business in England and Wales, the Landlord and Tenant Act 1954 is a huge piece of the puzzle. This Act grants what’s known as ‘Security of Tenure’—a tenant’s legal right to be offered a new lease when the current one ends. This is a powerful safety net, stopping a landlord from simply kicking you out to find someone who’ll pay more.

Security of Tenure is a default right for most UK commercial tenants. However, landlords often ask tenants to agree to ‘contract out’ of these protections, which removes this right completely.

Deciding whether to ‘contract out’ is a major business decision. You might get a lower rent or a better deal on other terms, but you give up the automatic right to renew your lease. Before you can agree to this, your solicitor must serve you with a formal notice explaining exactly what you're giving up. You have to carefully weigh the short-term benefits against the long-term security of knowing your premises are secure.

Lease Negotiation Tips and Common Pitfalls to Avoid

Stepping into lease negotiations without a clear plan is like walking into an exam unprepared—the outcome is unlikely to be in your favour. Whether you're a tenant or a landlord, getting the right terms takes more than a firm handshake. It demands solid preparation, a keen eye for detail, and knowing the common traps that can turn a good deal sour.

This knowledge helps level the playing field. It lets you approach the negotiating table with confidence, not apprehension. By learning what to push for and what to watch out for, you can secure a commercial lease agreement that truly supports your goals and helps you sidestep costly mistakes down the line.

Key Negotiation Strategies

Successful negotiation starts long before you sit down with the other party. It begins with good research and a clear list of what you want to achieve. Being prepared allows you to negotiate from a position of strength, not desperation.

Here are a few practical tips to get you started:

- Research Comparable Rents: Before you even think about making an offer, find out what similar properties in the area are leasing for. This market data is your strongest tool for making a fair offer and pushing back against an excessive asking price.

- Clarify All Additional Costs: The base rent is just one part of the financial picture. You need to insist on a detailed breakdown of all service charges and common area maintenance (CAM) costs. Vague phrases like "a fair proportion" should be swapped for specific percentages or fixed amounts.

- Negotiate Your Break Clause: An option to exit the lease early can provide critical flexibility if your business needs change. Always push for a break clause and scrutinise its conditions. Make sure the requirements for using it are clear, fair, and achievable.

A classic landlord tactic is to attach strict conditions to a break clause, making it nearly impossible to use. Ensure you have the right to end the lease without having to jump through an unreasonable number of hoops.

Common Pitfalls to Sidestep

Knowing what to ask for is important, but knowing what to avoid is just as crucial. Many commercial leases contain clauses that are heavily weighted in the landlord's favour. Spotting these potential issues before you sign is essential to protect your business.

One of the most dangerous areas is vague repair obligations. An FRI (Full Repairing and Insuring) lease could make you responsible for fixing problems that were there before you even moved in. Always get a professional survey done and attach a 'Schedule of Condition' to the lease. This document limits your liability to keeping the property in the state you found it, not paying to improve it.

Another critical point is the subletting clause. Your business could look very different in five or ten years. A restrictive clause that forbids you from subletting or assigning the lease can leave you trapped, paying for a space you no longer use. Make sure the lease allows you to sublet with the landlord's 'reasonable' consent.

If you do find yourself needing to get out of a lease, understanding the correct legal steps is vital. You can learn more about the process with a commercial lease termination agreement to see how it all works.

Frequently Asked Commercial Lease Questions

Diving into the world of commercial property can feel overwhelming. Whether you're a tenant trying to figure out your rights or a landlord needing clarity on your duties, getting simple, direct answers is crucial. Here, we tackle some of the most common questions that pop up when dealing with a commercial lease agreement.

Getting these basics right from the start helps you sidestep future confusion and costly disputes. It’s all about empowering you to make smarter decisions for your business, ensuring you know exactly where you stand.

What Is the Difference Between a Lease and a Licence?

This is a big one. A lease gives you exclusive possession of a property for a set period. Think of it like this: you get your own set of keys and the right to keep everyone out, even the landlord. This creates a legal interest in the property itself.

A licence, however, is much simpler. It’s just permission to use a space for a specific reason. You don’t get exclusive possession, and the owner can usually revoke it far more easily. Crucially, a licence doesn't give you the legal protections that come with a lease, such as the Security of Tenure found in the Landlord and Tenant Act 1954.

Do I Need a Solicitor for a Commercial Lease?

For straightforward, simple situations, a professionally drafted commercial lease agreement can be a great, cost-effective starting point. However, you should always get a solicitor involved for more complex or high-value agreements.

When you're committing to a long-term lease or a significant financial outlay, expert legal advice is essential to protect your interests. A good solicitor can spot risky or unfavourable clauses that a standard template might not account for.

What Happens When My Commercial Lease Expires in the UK?

What happens next all comes down to whether your lease is 'inside' or 'outside' the Landlord and Tenant Act 1954.

- Inside the Act: If your lease includes Security of Tenure, you typically have a legal right to ask for a new lease on similar terms. Your landlord can only refuse on very specific, limited grounds.

- Outside the Act: If you’ve formally agreed to contract out of the Act's protections, you have no automatic right to stay put. Once the term ends, the landlord can simply ask you to leave, and you’ll have no legal right to renew.

How Is Rent Reviewed in a Commercial Lease?

Rent is usually reviewed at set intervals, typically every three or five years, to make sure it stays in step with the current market.

The method for reviewing rent is a massive negotiation point, as it directly affects your business's future costs. The most common methods in the UK are an Open Market Rent Value (OMRV) review, where rent is adjusted to the going rate for similar local properties, or an index-linked review, where it's tied to an inflation measure like the Consumer Price Index (CPI).

Ready to create your own legal documents without the high cost and long waits? With Robot Lawyer, you can generate precise, expert-verified agreements in minutes. Start your free trial today and take control of your legal needs.