Mastering Risk Management in Contracts A UK Business Guide

Every business deal comes with a bit of a gamble. What happens if a client pays late, or a supplier just doesn't deliver? Contract risk management is all about looking at these "what ifs" head-on. It's the art of writing the rules of your business relationships to shield you when things don’t go to plan. The aim isn't to get rid of every single risk—that’s impossible—but to handle it smartly before it snowballs into a full-blown crisis.

What Is Risk Management in Contracts

It’s tempting to see a contract as just another piece of legal paperwork. A better way to think of it is as the blueprint for your business relationship. A good architect anticipates problems like heavy rain or unstable ground and builds in solutions—reinforced foundations, better drainage. Effective risk management in contracts does the exact same thing for your business.

It’s really just the practice of looking ahead, asking "what if?", and then embedding the answers right into your agreements. This proactive approach transforms your contracts from a potential source of arguments into a powerful tool for stopping them before they start.

Why It Matters More Than Ever

In today's unpredictable economy, sorting out contract risk isn’t just a task for big corporate legal teams anymore. For small businesses, freelancers, and landlords, it's become a core survival skill. The fallout from a single badly handled contract can be huge, causing cash flow nightmares, operational chaos, or expensive legal fights.

The market stats back this up. In the UK, the vendor risk management market—a key part of keeping contracts in check—is expected to more than double, growing from USD 1,017.6 million in 2024 to an estimated USD 2,385.0 million by 2030. Financial control owned a massive 37.73% market share in 2024, showing just how focused businesses are on nailing down financial risks in their agreements. You can read the full research about these vendor risk findings to see why solid contract strategies are becoming so crucial.

A contract should be a safety net, not a tightrope. The purpose of risk management is to ensure that if one party stumbles, the entire relationship doesn't collapse. It provides a clear, agreed-upon path to resolution.

This trend makes it clear: businesses are quickly realising their ability to stay afloat is directly linked to how strong their contracts are.

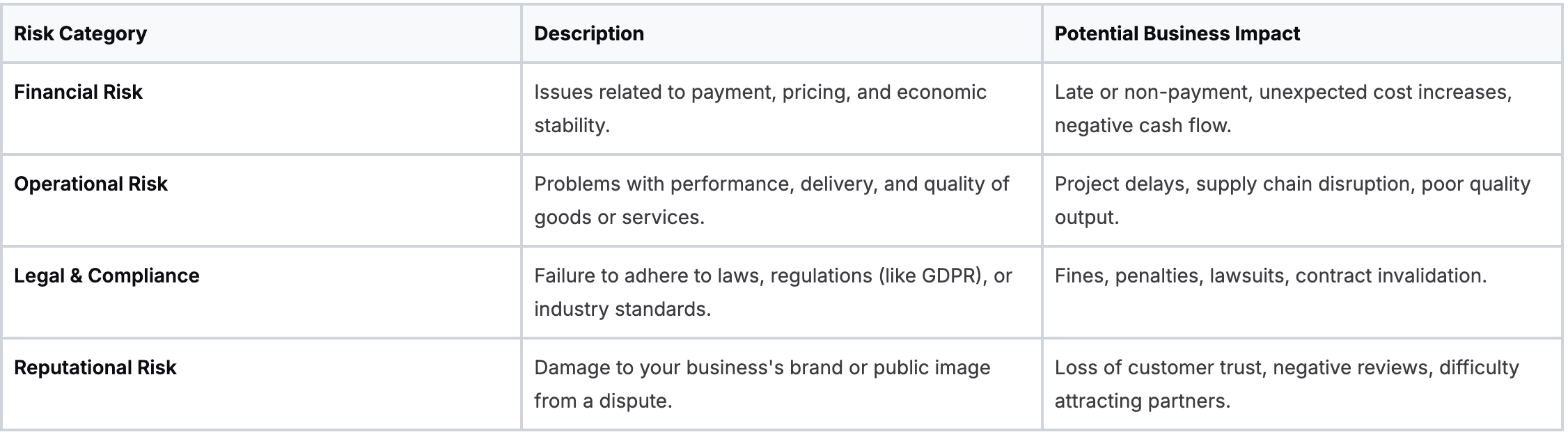

A Snapshot of Common Contractual Risks

The first step is knowing what you're up against. Most contract risks fall into a few main categories. Here’s a quick rundown of the most common ones and what can happen if they aren't managed properly.

Getting a handle on these different types of risk helps you spot potential weak points in your agreements before you sign on the dotted line.

Spotting the Most Common Contractual Risks

It’s one thing to talk about risk as a big, abstract concept. It’s another thing entirely to know what you’re looking for in the fine print of a contract. Effective risk management in contracts isn't about theory; it’s about spotting the real-world threats that can drain your bank account, disrupt your business, and tarnish your name.

Think of it like inspecting a house before you buy it. You aren’t just looking for "problems"—you’re specifically checking for a leaky roof, faulty wiring, or cracks in the foundation. In contracts, the same principle applies. The dangers hide in plain sight, often disguised as vague clauses, missing details, or one-sided terms. Let's break down the most common ones you’ll come up against.

Financial Risks: The Dangers to Your Cash Flow

Financial risks are the ones that hit you first and hurt the most. They directly impact your bottom line and can cause serious cash flow problems, particularly for smaller businesses and freelancers.

The biggest culprit is almost always ambiguous payment terms. A clause that just says "payment upon completion" should set off alarm bells. What does "completion" actually mean? Who has the final say? Without clear milestones, payment deadlines (like Net 30), and penalties for late payment, you're effectively letting the other party decide when—or even if—you get paid.

Keep an eye out for these other financial traps:

- Undefined Scope Creep: This is when the work keeps growing, but the fee doesn't. A vaguely written scope of work lets clients pile on extra tasks without any extra pay, killing your profit margins.

- Uncapped Costs: If you're the one buying, be wary of clauses that let suppliers increase their prices based on "market rates" or other fuzzy metrics. This can lead to sudden, unsustainable cost hikes you never saw coming.

According to a study by Deloitte, 1 in 5 organisations has faced a breach caused by a third party, and 1 in 10 has lost revenue because of it. Those financial losses often trace back to a weak spot in a contract.

Operational Risks: The Threats to Your Delivery

Operational risks are anything that stops you from running your business as you should. They mess with your performance, your delivery schedule, and the quality of your work. These risks can cause project delays and supply chain failures, which ultimately means you end up letting your own clients down.

Imagine you hire a supplier for a critical component. The contract lists a delivery date but has no specific service level agreements (SLAs) for quality or performance. If that component keeps failing, your whole production line could grind to a halt, but the contract offers you no clear way to hold them accountable.

Look for these operational red flags:

- Vague Deliverables: Phrases like "industry-standard support" or "reasonable efforts" are far too subjective. They are almost impossible to enforce if things go wrong.

- No Clear Timelines: Without firm deadlines for each stage of a project, accountability goes out the window, and delays become inevitable.

- No Clear Exit Strategy: What happens if the relationship goes sour? A contract with no clear termination clause can lock you into a failing partnership. Some situations might even demand specific legal steps, like those in a force majeure contract termination letter.

Legal and Reputation Risks: The Silent Killers

Legal and compliance risks are the easiest to ignore but can be the most catastrophic. They pop up when a contract doesn't follow the law, such as GDPR in the UK. If a vendor you've hired has a data breach because of their poor security, your business could be the one facing massive fines.

Then there’s reputational risk—the damage to your brand when a dispute or failure goes public. If a disagreement with a client gets ugly and ends in negative online reviews or a court battle, the long-term harm to your business’s credibility can be far more expensive than the original problem.

Both of these risks often spring from the same place: a contract that wasn't designed to handle conflict or failure in a professional and orderly way.

Building Your Defence with Key Contract Clauses

Knowing the risks is one thing, but actually defending against them is where the real power lies. The best risk management in contracts isn't some separate process; it happens right inside the document itself. Your strongest defence is woven directly into the clauses you negotiate before signing.

Think of these key clauses as specialised gear for your business. A firefighter wouldn't go into a blaze without a helmet and oxygen mask, and you shouldn't enter a business deal without the right contractual shields. Each clause protects you from a specific kind of danger.

This is your chance to stop passively accepting terms and start actively shaping them. Let's break down the most critical clauses and cut through the jargon to see what real protection looks like.

Capping Your Financial Exposure with Limitation of Liability

The Limitation of Liability (LoL) clause is probably the single most important financial safety net in any contract. Its job is simple but absolutely essential: to put a hard ceiling on the maximum amount of money you could have to pay if something goes wrong.

Without this clause, your liability is potentially unlimited. That means a single dispute could put your entire business—and sometimes even your personal assets—at risk. It’s a gamble no business can afford to make.

A well-drafted LoL clause turns an unknown, potentially catastrophic risk into a predictable and insurable figure. The wording here is everything.

The weak example is a blank cheque for disaster. The strong one sets a clear, quantifiable limit, making the risk a manageable business expense.

Transferring Blame with Indemnification Clauses

An indemnification clause, often called a 'hold harmless' clause, is a promise where one party agrees to cover the other party’s losses if a specific problem arises. In plain English, it’s about shifting responsibility for certain risks from your shoulders to theirs.

For example, if a client gets sued because the software you built for them infringes on someone else’s copyright, this clause would force the client to pay your legal fees and any damages. It works both ways. If you're using materials a client gave you and that leads to a lawsuit, you want them to indemnify you. You can find out more on how to build these protections in our guide to creating an Indemnity Agreement.

Key Insight: A fair indemnification clause is mutual. If you're asked to indemnify the other party for your mistakes, it’s only reasonable to ask for the same protection in return. One-sided indemnity clauses are a major red flag.

Handling the Unforeseeable with Force Majeure

What happens if something completely out of anyone’s control—a natural disaster, a pandemic, a global supply chain collapse—makes it impossible to do what the contract says? That's what a Force Majeure clause is for. It lets a party pause or end their obligations without being penalised for breaking the contract.

A weak clause will just vaguely mention "Acts of God." A strong clause gets specific. It will clearly define which events count and what the exact procedure is, like giving written notice within a set number of days. This stops the other side from using a minor delay as an excuse to get out of the deal.

Deciding How You'll Argue with Dispute Resolution

Even with the best contract in the world, disagreements can still happen. The Dispute Resolution clause sets the "rules of engagement" for how you'll solve them. This is your chance to avoid a public, expensive, and draining court battle.

This is a huge part of risk management in contracts because it directly controls the time, cost, and stress of a potential conflict. A strong clause will usually lay out a step-by-step process:

- Informal Negotiation: First, senior managers from both sides must meet and try to sort the issue out themselves.

- Mediation: If that doesn't work, you bring in a neutral third-party mediator to help find a compromise.

- Arbitration or Litigation: Only if mediation fails do you move on to binding arbitration or, as a final resort, litigation. This tiered approach can save a fortune in legal fees.

Even the UK government stresses the importance of using precise clauses to manage risk. Its own guidance points to indemnities and warranties and recommends capping supplier liability to control costs—a principle that's just as vital for businesses of any size. You can discover more insights about public sector contract risk on GOV.UK.

Creating Your Contract Risk Management Framework

A well-drafted contract is a great first step, but it’s really only half the battle. Even the most carefully worded clauses are useless if the agreement gets filed away and forgotten. To properly manage risk in contracts, you need a repeatable framework that turns good intentions into a solid business process.

Think of it like this: owning a top-of-the-range fire extinguisher is one thing, but having a full fire safety plan is another. The tool is vital, but the plan—knowing the exits, who to call, and how to actually use the equipment—is what truly keeps you safe. This framework is your business’s fire safety plan for its contracts.

The Four Stages of the Contract Risk Lifecycle

A solid contract risk framework doesn’t need to be over-engineered. It just follows a simple, logical lifecycle that you can apply to any agreement, whether it's for a freelancer or a major supplier. It all breaks down into four clear stages.

- Identification: First, you have to ask, "What could realistically go wrong here?" This means combing through the contract and thinking about the business relationship to spot potential financial, operational, and legal dangers before they have a chance to surface.

- Assessment: Once you've identified a risk, you need to size it up. Ask yourself, "How likely is this to happen, and how bad would the damage be?" This simple question helps you prioritise the threats that need your immediate attention.

- Mitigation: This is where you take action and decide, "What are we going to do about it?" You can mitigate risks directly in the contract by negotiating better terms, or you can do it at a process level by setting up new internal checks and balances.

- Monitoring: A contract isn't static; it's a living document. The final stage is about asking, "Are our protections still holding up?" It means regularly reviewing your agreements, tracking performance, and being ready to update terms when circumstances change.

Following this four-part cycle turns risk management from a one-off headache into a continuous, reliable system for your business.

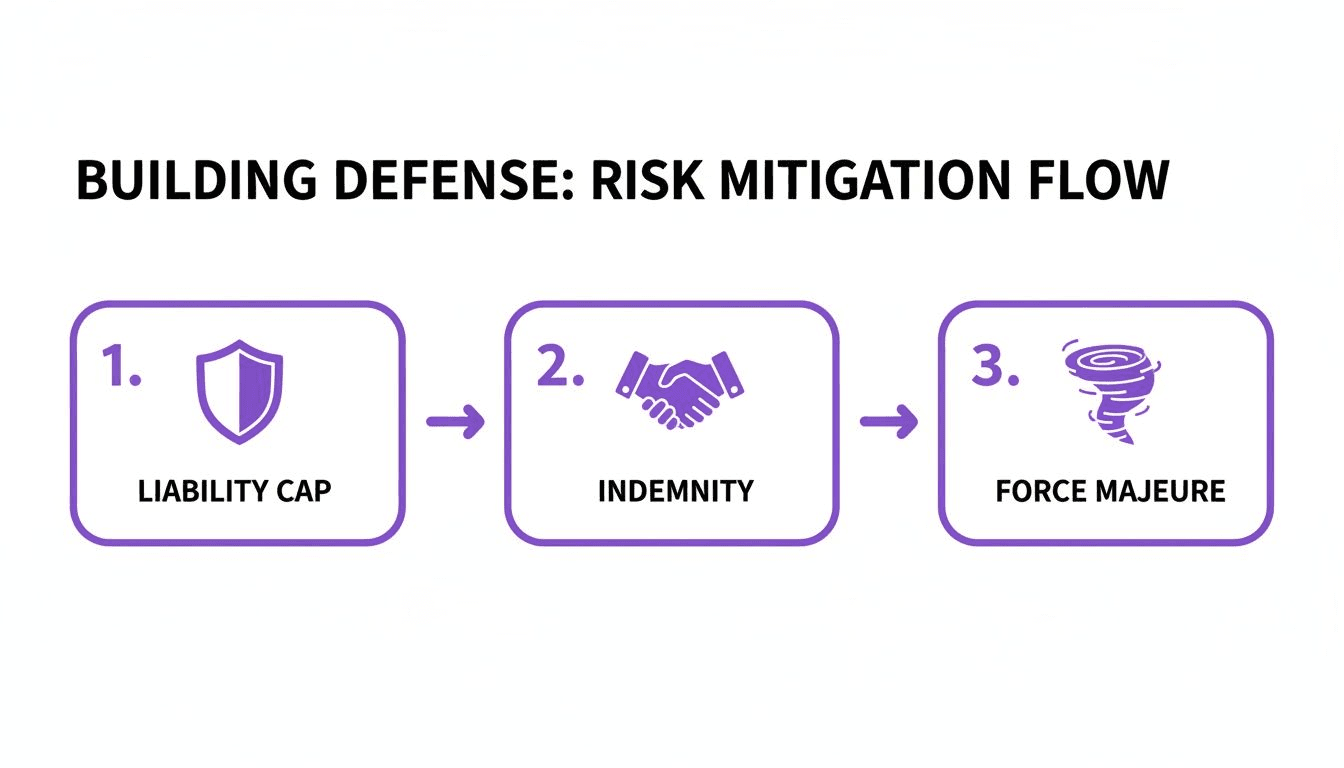

The diagram below shows some of the most powerful mitigation tactics you can build directly into your contracts.

As you can see, these defensive clauses function like shields, handshakes, and emergency exits, giving you multiple layers of protection against the most common contractual threats.

Essential Processes for Your Framework

Beyond these four stages, your framework needs some practical, day-to-day processes to make it stick. These are the habits that anchor your risk management strategy and make sure nothing falls through the cracks.

- Create a Central Contract Repository: It’s simple: you can't manage what you can't find. Keep all your active contracts in a single, organised place, whether that’s a secure cloud folder or a dedicated contract management system.

- Establish Clear Approval Workflows: Who actually has the authority to negotiate or sign contracts? Define a clear chain of command. This prevents rogue agreements and makes sure every contract gets a proper review from the right people.

- Set Automated Reminders: Don't leave it to memory. Use a calendar or project management tool to create alerts for key dates like renewals, termination notice periods, and performance reviews.

The need for structured controls like these is critical everywhere. Take the UK's social housing sector, for example. Intense financial pressures have made robust contract oversight a matter of survival. With key financial health metrics falling and sector debt soaring past £100 billion, boards are now required to monitor loan covenants within their contracts to prevent breaches that could cut off all financing. You can read more about these sector-specific risks on GOV.UK.

A contract risk framework isn't about creating more red tape. It’s about building clarity and control so your team can move forward with confidence, knowing they are backed by a consistent and reliable system.

By putting these processes in place, you create a system that not only helps you draft better contracts but also ensures they stay effective for their entire lifespan. This proactive approach is a cornerstone of building a resilient business and a core part of any effective Business Continuity Plan.

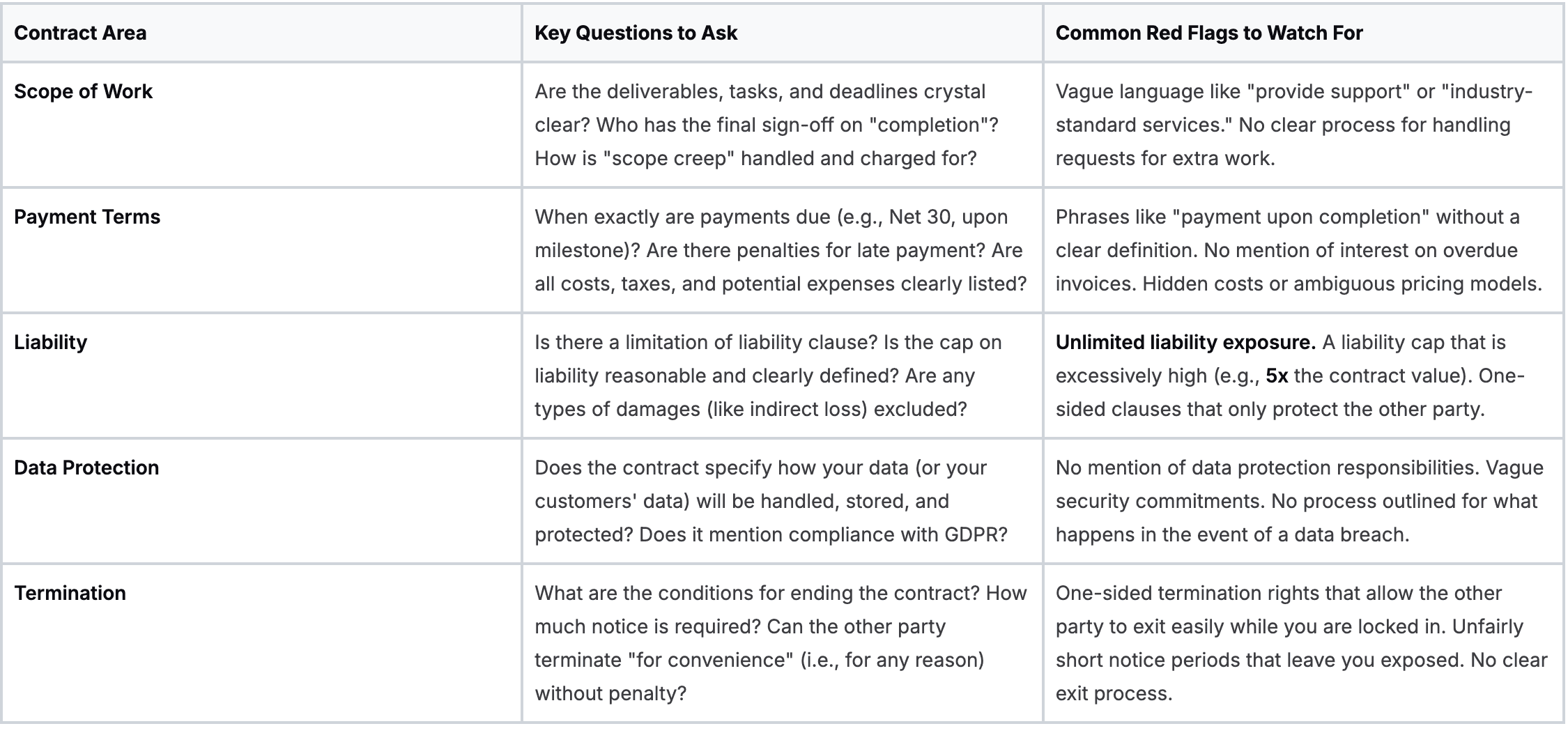

Your Practical Contract Review Checklist

Theories are great, but the real test of risk management in contracts is when a new agreement actually lands on your desk. This is where you move from theory to practice. Having a systematic review process is your best defence against hidden risks turning into costly problems.

To make it straightforward, we've put together a practical checklist you can pull out every time you review a contract. It zeroes in on the highest-risk areas and gives you the exact questions you need to be asking. Think of it as a pre-flight check for your business deals; it makes sure you’re secure before taking off.

This isn’t about trying to become a lawyer overnight. It’s about getting good at spotting the common traps and knowing when it’s right to push back or get an expert opinion. A structured approach means you can negotiate from a place of confidence and clarity.

Navigating the Negotiation

Before we jump into the checklist, let's reframe how you approach negotiation. It doesn't need to be a confrontation. It’s much more productive to see it as a joint effort to find a fair balance of risk that both sides can live with.

Negotiation isn't about winning or losing. It's about building a sustainable agreement where both parties feel protected and valued. A contract that heavily favours one side is often a recipe for future conflict.

When you spot an issue from the checklist, explain why it's a concern for you. Better yet, propose a fair solution. For instance, instead of flat-out rejecting an unlimited liability clause, you could suggest capping it at the total value of the contract fees. This collaborative style is far more effective and helps build a stronger, more trusting business relationship from the get-go.

Contract Red Flag Checklist

Use this table as your guide during the review process. It’s designed to help you quickly identify the most common red flags and high-risk terms that can lurk in any agreement.

This checklist gives you the power to take control of your contracts. It provides a logical, repeatable process for every agreement you face, ensuring that effective risk management in contracts becomes a core part of how you do business, not just an abstract idea.

Putting Your Contract Risk Management into Practice

So far, we’ve covered the 'what' and 'how' of managing risk in your contracts. You now know the types of risks to look for, the clauses that can protect you, and the right way to think about them. But knowing the theory is one thing; having the time and tools to actually do it is another entirely.

The reality for most UK businesses, freelancers, and landlords is that dealing with solicitors is often too slow, too complicated, and far too expensive. This leaves a dangerous gap. You know you need solid legal protection, but the cost and hassle can feel like a mountain you don’t have time to climb.

Making Proper Protection Accessible

The good news is that technology has stepped in to bridge this gap. Platforms like Robot Lawyer Limited are built specifically to solve these problems of cost, time, and complexity. They make robust contract risk management a realistic goal for everyone, not just big companies.

Instead of staring at a blank page or using a dodgy template you found online, you can access professionally prepared documents in minutes. These tools let you apply all the principles you've just learned in a practical, affordable way.

Effective risk management shouldn't be a luxury reserved for large corporations with in-house legal teams. It's a fundamental business need, and technology now makes it accessible to all.

How It Works in the Real World

Let’s look at how this plays out for different people across the UK:

- For the Freelance Designer: A designer can generate a legally sound services agreement in minutes instead of waiting days for a solicitor to draft one. They can lock in clear payment terms, a defined scope of work, and liability limits, protecting their income and preventing scope creep before a project even kicks off.

- For the Small Business Owner: Hiring and managing staff is a minefield of legal duties. A small business can create a compliant Contract of Employment with confidence, knowing they’ve met all legal requirements and clearly set out responsibilities. This drastically cuts the risk of future disputes with employees.

- For the Landlord: Trying to create a tenancy agreement without expert help is full of legal traps. A landlord can use a trusted platform to generate an Assured Shorthold Tenancy Agreement that’s fully compliant with current UK housing laws, protecting both their property and their tenant's rights.

When you use tools like these, you're not just creating a document. You are actively putting a risk management strategy in place. It transforms what was a daunting legal hurdle into a simple, confident step in your day-to-day operations.

Frequently Asked Questions About Contract Risk

When you start getting serious about risk management in contracts, a few questions always seem to pop up. Let's tackle some of the most common ones head-on, giving you the clarity you need to put these ideas into practice.

Can I Manage Contract Risk Without an Expensive Lawyer?

Yes, you absolutely can. For many day-to-day business agreements, the secret is to start with professionally drafted templates that are built to manage common risks from the get-go.

While a solicitor is non-negotiable for those high-stakes, multi-faceted deals, you can handle a huge chunk of your contractual risk on your own. Tools like Robot Lawyer give you that solid foundation, letting you create agreements like NDAs or service contracts confidently, without the usual legal fees and hold-ups.

What Is the Single Biggest Risk in a Small Business Contract?

Vagueness. Hands down. Ambiguity, especially around the ‘Scope of Work’ and ‘Payment Terms’, is the number one cause of disputes. A contract that isn't perfectly clear on what will be done, by when, and for how much is simply asking for trouble.

Ensuring these sections are crystal clear is the most powerful risk mitigation action you can take. A vague contract is an argument waiting to happen.

How Often Should I Review My Existing Contracts?

A contract isn’t a ‘set it and forget it’ document. For any ongoing or long-term agreement, a yearly review is a sensible baseline.

You also need to pull that contract out for an immediate review if there are any major changes, such as:

- Your business operations or structure changes.

- The other party’s situation changes (e.g., they get acquired).

- Relevant laws are updated, like data protection regulations.

Set a calendar reminder. Make it a habit. This kind of proactive monitoring is at the very heart of effective risk management in contracts.

What Is a Limitation of Liability Clause?

Think of it as your financial safety net. This clause puts a firm cap on the maximum amount of money you could be liable for if something goes wrong.

Without one, your business could be on the hook for unlimited damages from a single dispute, which could be catastrophic. A well-drafted limitation of liability clause turns an unknown, terrifying threat into a known, manageable business risk. It’s one of the most critical risk management tools in any agreement you’ll ever sign.

Don't let contract complexity leave you exposed. With Robot Lawyer, you can generate legally sound documents in minutes, putting robust risk management well within your reach. Create your first secure contract today.