How to Make a Will in the UK Your Definitive 2026 Guide

Making a will is one of those things we all know we should do, but it’s so easy to push to the bottom of the list. In reality, it's the only way to make sure your wishes are legally binding after you’re gone. It’s your instruction manual for everything you leave behind—listing your assets, naming who gets what (your beneficiaries), and choosing a trusted person to handle it all (your executor). Getting this document signed and witnessed correctly is the single most important thing you can do to protect your family's future.

Why You Need a Will in 2026

Create a Free Will and Testament Here!

Let's face it, nobody enjoys thinking about a time when they won't be around. But heading into 2026 without a will means you’re leaving your life’s work—and your loved ones’ financial security—entirely up to chance.

If you die without a will, the law steps in with a rigid set of instructions known as the Rules of Intestacy. These rules are completely impersonal and often don't reflect what you would have actually wanted.

The Real Impact of Intestacy Rules

The intestacy framework is notoriously outdated and often leads to devastating outcomes for modern families, as it strictly prioritises spouses and direct descendants.

- Unmarried Partners: If you have a long-term partner but aren't married or in a civil partnership, they have no automatic inheritance rights. They would be forced to make a costly and emotionally draining legal claim against your estate just to get what you may have intended for them.

- Blended Families: The rules could mean your entire estate passes directly to your current spouse. This could unintentionally disinherit children from a previous relationship, leaving them with nothing.

- Separated but not Divorced: Are you separated but not yet legally divorced? Your estranged spouse could still inherit a huge chunk of your estate, which is rarely what people want in that situation.

A will is your voice after you are gone. It replaces the cold, one-size-fits-all rules of intestacy with your personal, considered decisions, ensuring the people you care about are looked after exactly as you intend.

Beyond Property: The Rise of Digital Assets

These days, our assets go far beyond just a house or a bank account. Your will is now a crucial tool for managing your digital footprint, which can include anything from cryptocurrency and online share portfolios to social media accounts with huge sentimental (or even financial) value. Without clear instructions, these digital assets can easily be lost for good.

Thankfully, people are waking up to these risks. The UK Wills & Probate Consumer Research Report 2025 revealed that, for the first time ever, over 40% of UK adults now have a will. This shift is happening because more people understand the dangers of intestacy and have access to new, easier options. In fact, solicitors' market share recently dropped below 50% as online will-writing services have become more popular.

Learning how to make a will isn't just about ticking a legal box; it's an act of care that gives your family clarity and security when they need it most. While a will covers what happens after you're gone, you might also want to plan for who makes decisions if you're unable to. You can learn more by checking out our guide on Lasting power of attorney .

Valuing Your Estate and Choosing Beneficiaries

Create a Free Will and Testament Here!

Before you can decide who gets what from your will, you need a crystal-clear picture of what you actually own. This first step – figuring out your estate's total value – is the bedrock of a solid will. Think of it as creating a personal balance sheet; it’s about far more than just your house and a savings account.

Getting this valuation right is crucial for everything that comes next. It affects potential Inheritance Tax calculations and ensures your gifts can be distributed as you intended. It takes a bit of honesty and some detective work, but it’s the only way to make sure your will truly reflects what you have.

Compiling Your Asset Inventory

First things first, let's list your most significant assets. This will include the obvious things like property, vehicles, and the money you have in the bank. But a really thorough inventory goes much deeper.

To build a complete picture, you’ll need to think about every corner of your financial and personal life. Consider these common categories:

- Property: This is your home, any buy-to-let properties, or land you might own. It's wise to get a realistic market valuation.

- Financial Assets: This covers a wide range – from ISAs, premium bonds, and shares to pensions and any life insurance policies that pay out on your death.

- Personal Belongings: Think about items with high monetary or sentimental value. This could be jewellery, art, antiques, or other valuable collections.

- Digital Assets: This is an increasingly important area that's easy to overlook. It includes things like cryptocurrency, valuable domain names, or even online accounts that generate an income.

Don’t forget to tally up your liabilities, too. These are things like mortgages, loans, and credit card debts. Your net estate is what’s left after these debts are settled, and this is the figure your will ultimately deals with.

A common mistake I see is people only focusing on major assets like their house. Forgetting smaller pots of money, pension death benefits, or even valuable digital accounts can cause real confusion down the line. It can mean your main beneficiaries end up with much more, or less, than you intended.

Demographics play a big part in what people prioritise. Recent analysis shows that nearly 50% of people now consider investments their most important asset, which highlights a real shift in financial planning. This data also reveals that men are almost 5% more likely than women to have a will. Interestingly, will-making reluctance is still widespread, with only 4% in one sample having a will, though many more are planning to create one. You can explore more about these will-making statistics to understand the trends.

The Personal Task of Choosing Beneficiaries

Once you have a clear inventory, the next step is deciding who you want to leave your assets to. These people, or organisations, are your beneficiaries. This is a deeply personal decision, and there are no right or wrong answers—only what feels right for you and your family.

You might have a simple structure in mind, like leaving everything to your spouse or children. For instance, a very common setup is leaving the entire estate to a surviving partner, with the understanding that it will then pass to the children after their death.

Alternatively, you may have more specific wishes.

- Specific Gifts (Legacies): You could leave a specific sum of money, say £5,000, to a grandchild for their education. Or you might want to give a particular piece of jewellery to a close friend. These are known as legacies.

- Charitable Donations: Leaving a gift to a charity is a wonderful way to support a cause close to your heart. This can be a fixed amount or a percentage of your estate.

- Residuary Estate: This is the "everything else" pot. After all debts, expenses, and specific gifts are paid, whatever is left over is your residuary estate. You need to name who receives this, and it’s often the most significant part of a will.

If you have young children or a loved one who might struggle to manage a large inheritance, you can also use your will to set up a trust. This allows you to appoint trustees to manage the assets on their behalf until they reach a certain age or another milestone. It gives you peace of mind and ensures your legacy is handled exactly as you planned.

How to Draft the Key Clauses in Your Will

Now for the crucial part: turning your decisions about assets and beneficiaries into a legally sound will. This is where you put your plans into action, creating the specific instructions that will guide your executor.

Think of these clauses less as stuffy legal jargon and more as a clear, precise instruction manual you're leaving for the people wrapping up your affairs. Getting the wording right here is your best insurance policy against confusion and family disputes down the line.

Let's break down the essential building blocks you'll need.

Starting With a Clean Slate

Before you can lay out your new wishes, you have to wipe the slate clean. The very first active clause in your will needs to be a revocation clause. It’s a simple but vital sentence that cancels any previous wills or codicils (official amendments) you’ve ever made.

This is a legal reset button, and forgetting to press it is a common and costly mistake. If you don't include this, an old, forgotten will could emerge and create a legal nightmare for your loved ones while the courts try to figure out which one is valid.

Sample Wording: "I hereby revoke all former wills and testamentary dispositions made by me and declare this to be my last will and testament."

This single line makes it clear that this document, and only this one, represents your final wishes. It gives your executor a clean, undisputed starting point.

Defining Your Specific Gifts and Legacies

Once the old documents are revoked, you can start detailing your specific gifts, which are known legally as legacies. This is where you set aside particular items or sums of money for individuals or charities.

Absolute clarity is your goal here. Vague descriptions are a recipe for arguments over what you really meant.

- Pecuniary Legacies (Cash Gifts): Be direct and unambiguous. For example, "I give the sum of £5,000 to my nephew, James Smith."

- Specific Legacies (Items): Describe items with as much detail as possible. Don't just say "my watch"; instead, write "my silver Omega Seamaster watch with the blue dial." This is crucial if you own more than one.

- Charitable Gifts: Always use the charity's full registered name and, if possible, its registered charity number. This ensures your gift doesn't get lost or sent to the wrong organisation.

Imagine you're leaving your grandmother’s engagement ring to your daughter. You need to be specific: "I give my gold diamond solitaire engagement ring, which previously belonged to my mother, to my daughter, Sarah Jones." That level of detail leaves no room for doubt.

After you've listed these specific gifts, you need a plan for everything else.

The All-Important Residuary Clause

This might just be the most important clause in your entire will. The residuary clause is a catch-all that deals with whatever is left of your estate after all your debts, funeral costs, taxes, and specific legacies have been paid out.

This "everything else" is called the residue or residuary estate, and it's often the largest part of what you own. Without a residuary clause, anything not specifically mentioned in your will could be treated as if you died without a will at all (intestate), which could mean it goes to people you never intended.

You might, for instance, leave the entire residue to your spouse or partner. Or you could instruct your executor to split it equally between your children.

Sample Wording: "I give the whole of my estate (both real and personal) not otherwise specifically disposed of by this my will, after payment of my debts, funeral and testamentary expenses, to my wife, Jane Doe, absolutely."

This clause is your safety net. It covers assets you might have forgotten or even assets you acquire after writing the will. It’s the final instruction that ensures every last bit of your estate is handled exactly as you wish. If you want to make sure you get these clauses exactly right, a professionally drafted Last Will and Testament can provide a solid and reliable framework.

Appointing an Executor for Your Estate

Choosing who will act as your executor is one of the most critical decisions you'll make when writing your will. This person, or in some cases a professional firm, is legally on the hook for carrying out your exact wishes. It’s a role that demands absolute trust, serious organisational skills, and the emotional strength to handle what can be a very bumpy road.

The executor's job kicks in the moment you’re gone. They are responsible for the entire administration of your estate, and believe me, it’s no small task. This means gathering up all your assets, figuring out their total value, and then settling any outstanding debts and taxes. Only after all that is sorted can they finally distribute what’s left to the people you named in your will.

Family Member vs Professional Executor

Most people instinctively turn to a spouse, an adult child, or a close friend. It makes sense—they know you well and have a personal stake in seeing your wishes respected. But this well-trodden path can be littered with unexpected pitfalls.

Imagine you appoint your two children as joint executors. If their relationship is already a bit rocky, the pressure of managing your estate can easily fan the flames of old disagreements. Suddenly, simple decisions like selling the family home or valuing sentimental items can become sources of bitter conflict, stalling the whole process and potentially wrecking family harmony for good.

The role of an executor is not a ceremonial title; it is a demanding job. The administrative burden can be immense, involving complex paperwork, dealing with financial institutions, and adhering to strict legal deadlines. It is an act of kindness to consider whether your loved one truly has the time, skill, and emotional resilience for the task.

The alternative is appointing a professional, like a solicitor or a dedicated probate firm. Yes, this comes with a fee, but what you’re paying for is impartiality and deep expertise. A professional executor isn’t going to get tangled up in family drama. They are experienced in navigating all the legal and financial hurdles with cool-headed efficiency.

This option is particularly smart if your estate is complicated, perhaps involving a business, trusts, or assets located overseas. It takes a huge weight off your loved ones' shoulders when they are already grieving.

What to Look For in an Executor

Whether you lean towards a family member or a professional, there are certain non-negotiable qualities you need to look for. Think of it as hiring for the most important job you'll ever need to delegate.

Your ideal executor should be:

- Trustworthy: This is the absolute foundation. You're entrusting them with your entire life's work.

- Organised: They'll be juggling stacks of paperwork and keeping track of numerous financial details.

- A Clear Communicator: The executor needs to keep all the beneficiaries in the loop, manage their expectations, and handle any disagreements with tact and diplomacy.

- Resilient: They might have to face down difficult beneficiaries or sort out unexpected legal complications.

Once you have someone in mind, you must sit down and have an open conversation with them. Lay out exactly what the job entails and ask if they are genuinely willing and able to take on the responsibility. Just naming them in your will without their consent is a recipe for disaster. This simple chat ensures they are prepared and gives you the chance to find someone else if they say no, saving your family a massive legal headache down the line.

How to Legally Sign and Witness Your Will

You’ve done the hard part – deciding who gets what and drafting your will. But all that effort means nothing if you fall at the final hurdle. This is the moment that turns your wishes into a legally binding document, and getting it wrong can make the entire will invalid.

The rules for signing, laid out in the Wills Act 1837, are strict for a reason. You must sign your will (or acknowledge your signature) while two independent witnesses are physically in the room with you, and with each other. They then need to sign it in your presence. Think of it as a small, formal ceremony where everyone is present and watching.

Who Can Be a Witness?

Choosing your witnesses isn't something to take lightly. The law is very specific here to prevent any conflicts of interest or accusations that you were pressured into signing.

Your witnesses must meet these criteria:

- Be aged 18 or over.

- They cannot be a beneficiary in your will.

- They cannot be the spouse or civil partner of a beneficiary.

If a beneficiary or their partner does witness your will, they will be completely cut out from inheriting anything. The will itself might still be valid, but their gift will fail. It’s a simple mistake with devastating consequences for a loved one.

The safest bet is to ask someone you trust who has zero financial interest in your will. A neighbour, a friend, or a work colleague are all excellent choices. They don't need to read the will or know what’s in it—their only job is to confirm they saw you sign it.

The Signing and Attestation Process Checklist

To make sure everything is watertight, you need to follow this sequence exactly. The order of these steps is absolutely critical.

- Get Everyone Together: You and your two witnesses must all be in the same room for the entire signing process.

- You Sign First: While both witnesses are watching you, sign the will.

- The Witnesses Sign: Immediately after, each witness must sign the will in your presence. It’s also good practice for them to print their full name, address, and occupation.

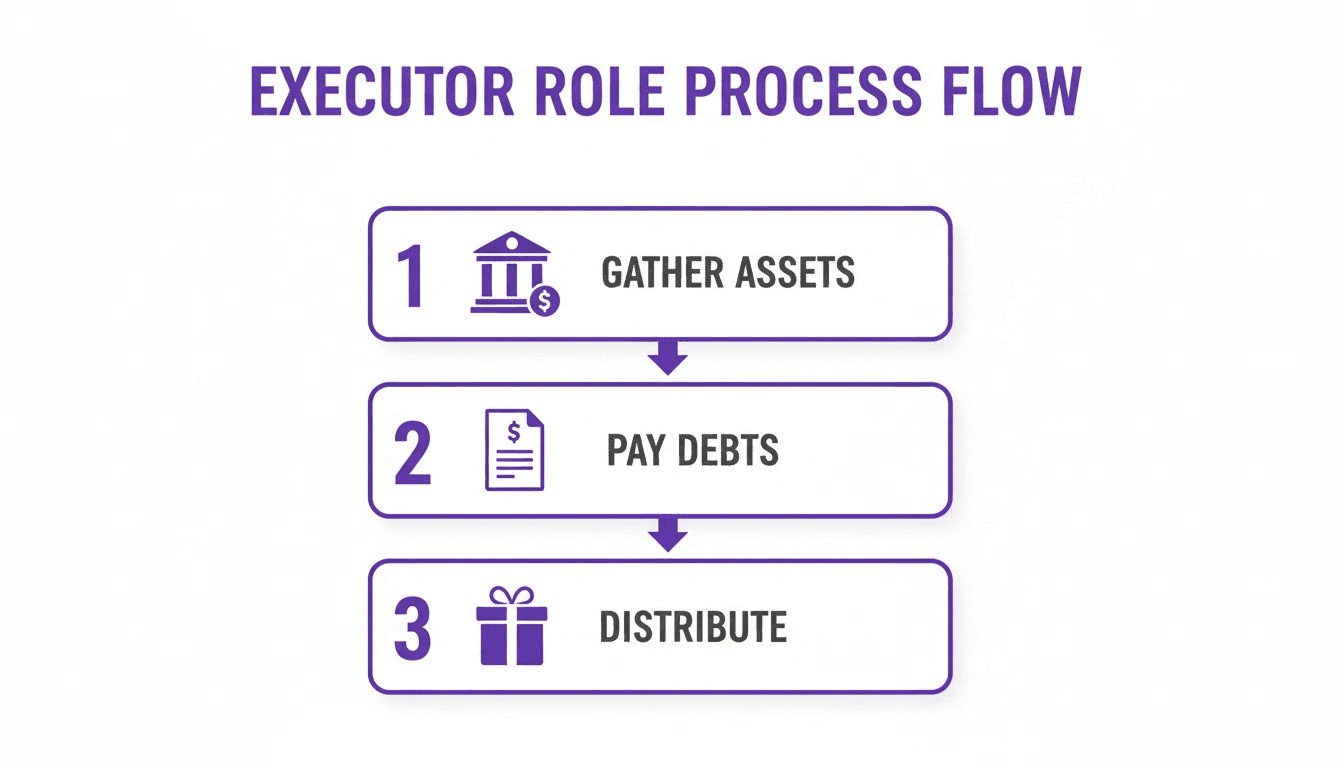

Once your will is signed and valid, your chosen executor will eventually follow a clear process to carry out your instructions.

Create a Free Will and Testament Here!

This visual breaks down the executor's core responsibilities into gathering assets, paying off any debts, and finally, distributing what’s left to your beneficiaries.

The Future of Signing Wills

For now, the traditional pen-and-paper method is the only legally secure way to sign your will in the UK. But the world is changing, and the law is slowly starting to catch up.

Shockingly, recent research found that 25% of people don't even know where to begin with making a will. This is a huge problem, especially when 70% of us are mainly motivated by making sure our assets go to the right people. This gap has opened the door to digital solutions, with 36% of people now open to a fully electronic will, not far behind the 39% who still prefer paper.

These evolving attitudes are reflected in ongoing proposals from the Law Commission to modernise will-making, which could one day allow for electronic signatures with strong safeguards. You can read the full research about these evolving attitudes to will-making to see how public opinion is shifting.

Storing and Updating Your Will Over Time

You’ve gone to the trouble of writing your will, which is a massive step. But don't just file it away and forget about it. Think of your will not as a static, one-off document, but as something that needs to be kept safe and checked in on throughout your life. How you store it and when you update it are just as important as getting the wording right.

Once it’s signed, that original document is gold. It needs to be kept somewhere safe where your executor can actually find it when the time comes. If the original gets lost, damaged, or destroyed, it could be as if you died without a will at all, which would undo all of your careful planning.

Where to Keep Your Will Safe

So, where should you keep this vital document? You have a few options, each with its own set of risks and benefits.

Tucking it away in a desk drawer at home is obviously the free and easy choice, but it's also the riskiest. It could easily be thrown out by mistake during a clear-out, get damaged in a house fire or flood, or even be hidden or destroyed by a family member who isn't happy with its contents.

A far more secure route is to have it stored by the solicitor who helped you write it, or with a specialist will storage company. This ensures it’s kept in a professional, fireproof facility. The only real drawbacks are the potential annual fee and making sure your executor knows exactly which firm has it.

Another option that's become quite popular is lodging it with the National Will Register. It’s important to realise they don't store the physical document itself. Instead, they record its location. This service makes it incredibly straightforward for your executor to track it down, regardless of where you’ve actually stored it.

The key to storing your will is finding the right balance between security and accessibility. Your executor needs to be able to find it without a drama, but it also has to be protected from loss and damage. No matter which option you choose, always tell your executor where the original is.

When to Review and Update Your Will

Your will needs to keep pace with your life. Big life events can have a huge impact on your financial and personal situation, often making parts of your will out-of-date or, in some scenarios, completely invalid.

Get into the habit of reviewing your will every three to five years, and always pull it out for a check-up immediately after any major life change. The most common triggers for a review include:

- Getting Married: In England and Wales, getting married or entering a civil partnership automatically revokes an existing will. The only exception is if the will was specifically made 'in contemplation' of that marriage.

- Divorce or Separation: Divorce doesn't revoke the entire will, but it does change things. Your ex-spouse is typically treated as if they had died before you, which could cause gifts to fail or pass to people you didn't intend.

- Having Children or Grandchildren: You’ll almost certainly want to add new members of the family as beneficiaries.

- A Major Financial Change: Coming into a large inheritance, buying a significant property, or selling a business can all change the shape of your estate and require a rethink.

- The Death of a Beneficiary or Executor: If someone named in your will passes away, you'll need to amend it to appoint replacements and decide where their gift should go.

For a very small change, like updating an executor or changing a small cash gift, you can use a simple legal amendment known as a codicil. Be careful, though. For anything more substantial, it’s almost always safer and clearer to just write a completely new will. If you're weighing your options for a minor tweak, you can learn more about creating a codicil to see if it's the right move for you.

Common Questions About Making a Will

Once you've decided to write your will, it's natural for a few common questions to pop up. It's a big task, and getting clear answers is the best way to move forward with confidence.

Let's walk through some of the most frequent queries we hear from people just like you.

Can I Write My Own Will Without a Solicitor?

Yes, absolutely. You can write your own will, and as long as it's drafted, signed, and witnessed correctly, it is completely legal. This is often called a DIY will.

For many people with straightforward finances and a simple family setup, using an online will-writing service or a good quality template is a brilliant, cost-effective way to get it done. It's fast and gives you peace of mind.

However, things change if your situation is more complex. In that case, getting professional legal advice isn't just a good idea—it's essential.

You really should see a solicitor if your estate includes:

- Business or agricultural property.

- Any property located overseas.

- Complex family dynamics, like blended families or dependents who need ongoing care.

- The need to set up a trust to protect certain assets.

A solicitor helps you navigate these tricky areas, steering you clear of costly mistakes, unexpected inheritance tax bills, and the risk of your will being challenged later on.

What Happens If I Die Without a Will?

If you pass away in the UK without a valid will, the law steps in. Your estate is then shared out according to what's known as the Rules of Intestacy. These are rigid, impersonal rules that determine who gets what, based on a fixed family tree.

The Rules of Intestacy often fail to reflect modern family life. For instance, an unmarried partner is entitled to nothing under these rules, regardless of how long you were together. They would have to make a stressful and expensive legal claim against your estate.

The rules automatically prioritise spouses, civil partners, and children. If you have no surviving relatives at all, your entire estate goes to the Crown. The only way to make sure your assets go to the people and causes you care about is to make a will.

How Much Does It Cost to Make a Will?

The cost really depends on the path you take. A simple will made with an online service is by far the most affordable choice, often costing less than £100.

If you go to a solicitor for a straightforward will, you can expect to pay somewhere between £200 and £500. For more complex estates that need specialist advice—perhaps on trusts or inheritance tax planning—the costs can easily go above £1,000.

At Robot Lawyer, we make creating legally sound documents straightforward and affordable. Generate your customised will in minutes and get peace of mind today.